Musings

Inflation Up, Rates Up

When the Trump Administration nominated Kevin Warsh to replace Jerome Powell as the chairperson of the Federal Reserve Board, many expected a quick announcement that the Fed would be slashing the Fed Funds rate. The tea leaves were not hard to read: President Trump demanded an aggressive rate cut, and repeatedly berated—and even criminally investigated—former Chairperson Powell for not complying. His hand-picked successor understood the assignment.

The Perils of Prediction

If you want to place a bet that the Sun won’t rise tomorrow, or (less likely) that the Cleveland Browns will dominate the next Super Bowl, you can turn to the prediction platform called Polymarket. People who believe something will happen—literally anything—can make a bet, like the $200 million wagered on whether Ukrainian President Volodymyr Zelensky would wear a suit at his next meeting, or the $1.3 million that was bet on whether Donald Trump would say the word ‘hottest’ during a recent meeting with UK Prime Minister Keir Starmer. Speculative markets have emerged for the return of Jesus Christ, the existence of aliens and whether the Earth is flat.

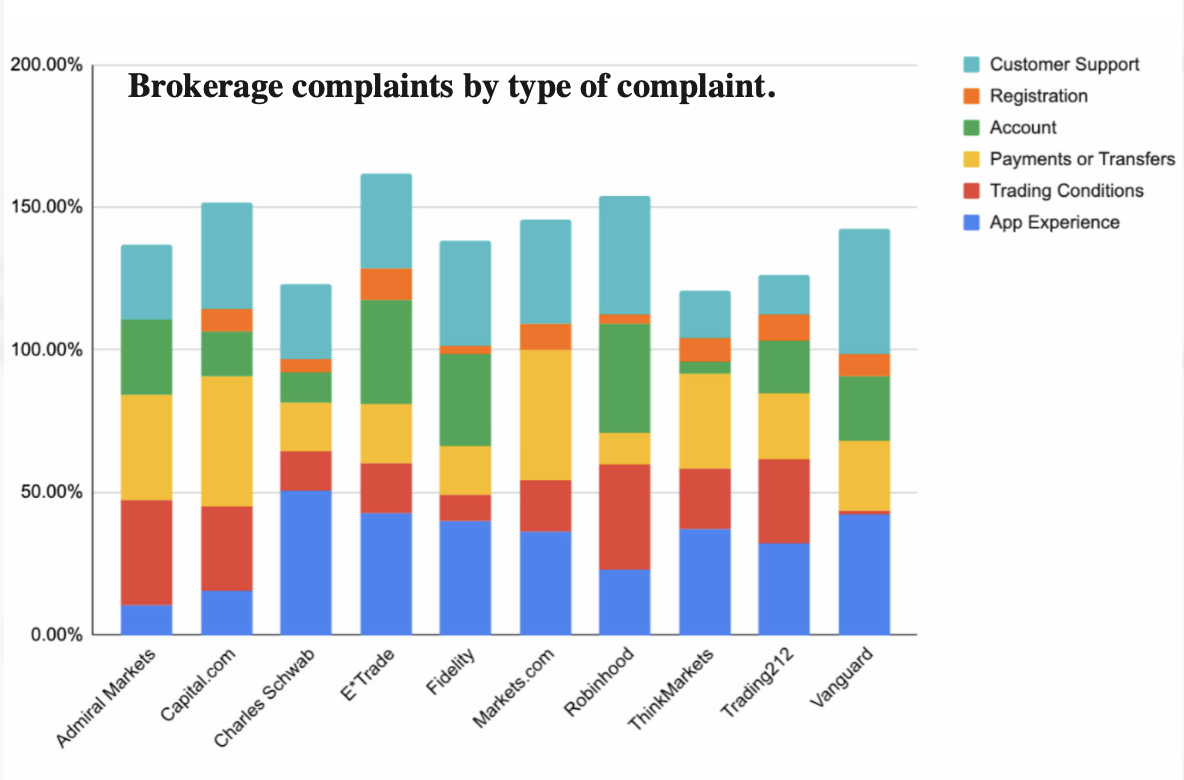

Complaints Chronicle

Discount and retail brokerage firms have run advertisements suggesting that their customers could trade their way to buying their own private island or massive riches, but the reality is that few active traders avoid losing their nest egg, much less earn above-market gains. But now these traders have new complaints, which suggest that it’s not just safer, but also more convenient to rely on a professional.

Leveraged to the Hilt

If you’re just now returning from the Moon, then you might not have heard about the turmoil at CBS, where Stephen Colbert has hosted his last Late Show episode, where 60 Minutes seems to get a new remake every month or so, and CNN anchors worry that their independence—such as it is—are about to go the way of the passenger pigeon.

An Independent Decision

The most recent Federal Reserve Open Market Committee announcement came as no surprise: the Fed held the fed funds target steady, meaning that short-term interest rates won’t be going up or down due to the central bank’s policy. What WAS a surprise, however, is that Fed chairman Jerome Powell announced that he isn’t going anywhere.

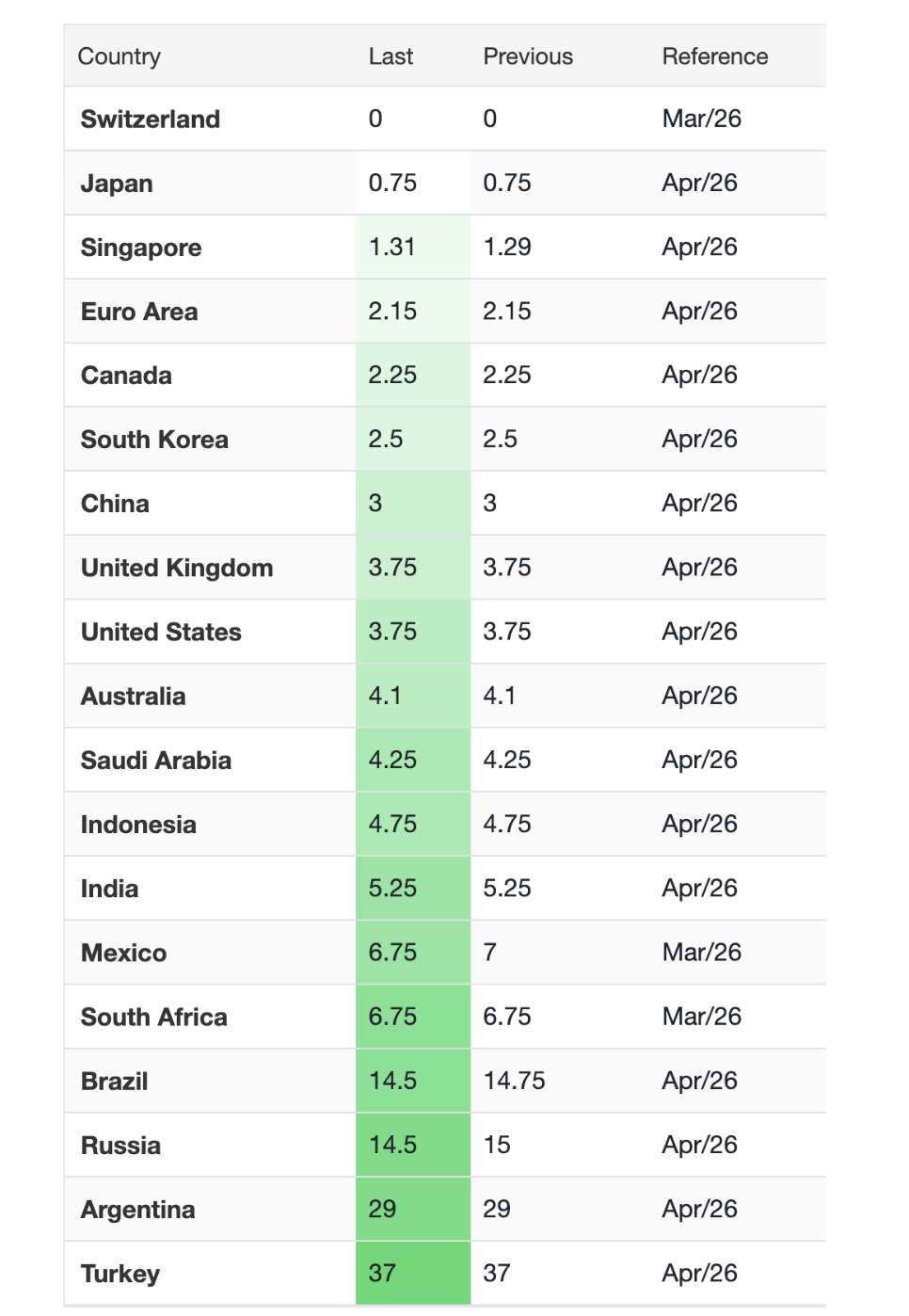

Rates Around the World

America’s short-term interest rates of 3.5% to 3.75% might seem a bit high—until you compare them to the 37% rate that Turkish companies and citizens are expected to pay—due, of course, to that country’s extraordinarily high inflation rate. Argentinians are currently paying off short-term loans at a 29% rate. Russians, whose economy is experiencing a number of challenges currently, pay 15%.

Covid in the Rear View Mirror

If you think we’re finally past the Covid pandemic, well, you may be right. The chart comes from the Center for Disease Control, which shows the number of deaths per 100,000 population going back to the start of the epidemic. As you can see, the death rate looks like a fading heartbeat, getting weaker and weaker as it trends toward zero. The hospitalization rate shows a similar trend, suggesting that the symptoms have become weaker as the disease mutates—to the point where only 0.4% of hospitalizations are now Covid-related.

Cheap—and Expensive—at the Pump

…The U.S. is now the world’s leading petroleum producer, yet its gas prices are somewhere near the middle of the pack, far below Egypt, Kuwait, Qatar, Saudi Arabia, Oman and Iraq (all below $2.50 a gallon).

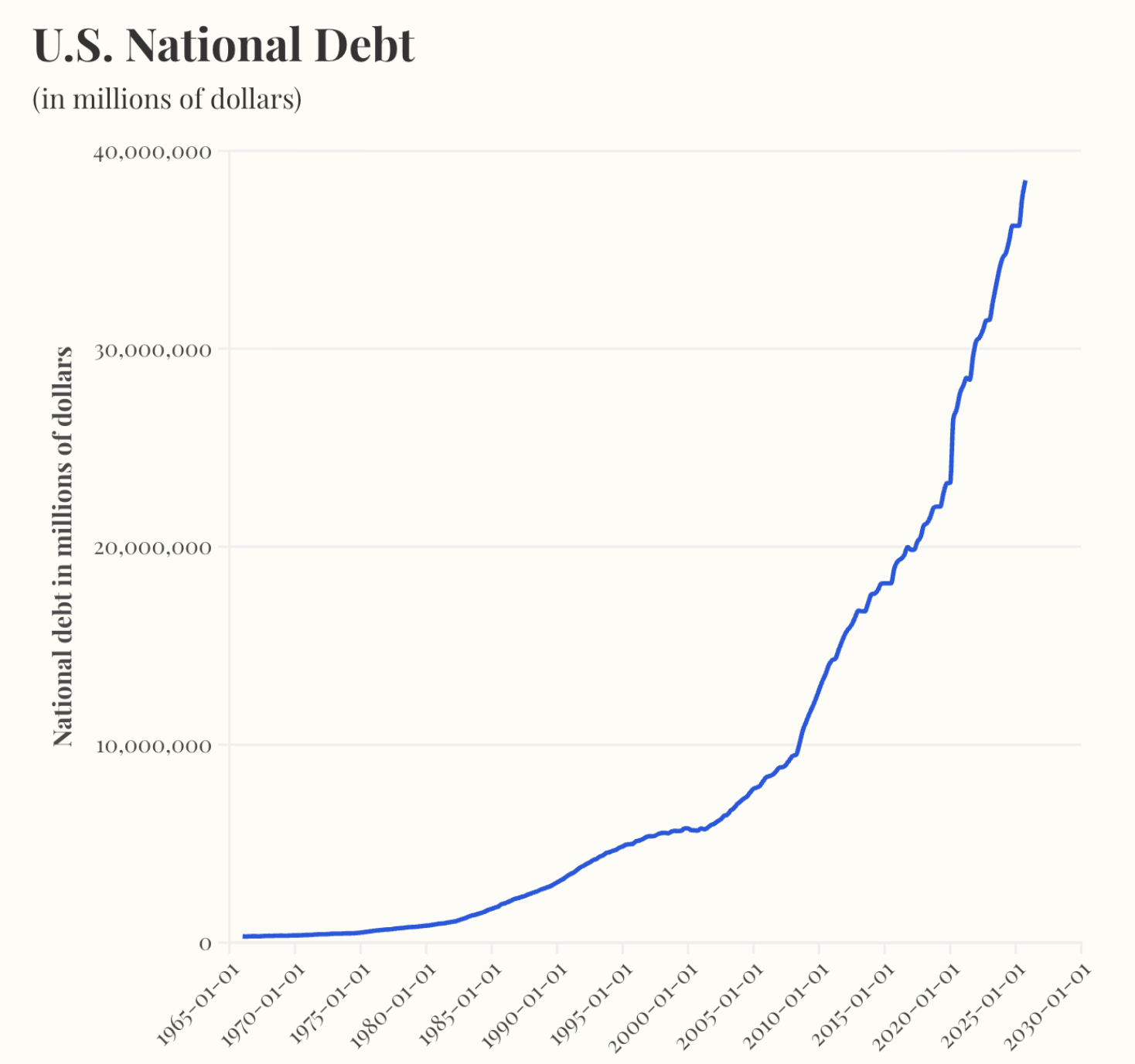

Debt and Politics

Looking ahead to the November elections, one headline that is bound to surface is the national debt. According to the Peterson Foundation, the U.S. debt figure will pass $40 trillion by November, and is now growing by roughly a trillion dollars every five months. Last month, the Congressional Budget Office estimated that this year’s balance sheet alone will bleed red to the tune of $1.9 trillion. Under current law, the annual debt increase will come to $3.1 trillion in 2036.

2026 First Quarter Investment Report - Is the Bull Market Over?

If you look at the quarterly results as a whole, the returns so far have been roughly flat, with small losses or gains depending on the asset class. But March was a brutal month for the equities markets, which suggests that the markets are experiencing downward momentum that is largely hidden by the quarterly returns.

Oil Shock Equals Market Turbulence

The war in Iran has led to an alarming spike in oil prices, from $65 a barrel before the U.S./Israel attacks to roughly $115 as you read this. It’s not an exaggeration to call this an ‘oil shock,’ and some of the shock is felt when people refuel their cars at $4 to (in parts of California) $6 a gallon.

Rates Down. Sales Up?

Is it time to refinance your home mortgage? U.S. mortgage rates have taken an unexpected dip, to an average 6.09%, reaching their lowest level since 2022. The rate on 5-year adjustable mortgages fell to 5.23%.

The Two Faces of AI Anxiety

The investment markets have been jittery of late, and the headlines have blamed something called ‘AI anxiety.’ But what, exactly, does that mean, and is it a legitimate worry?

Crypto Crisis

The cryptocurrency world is experiencing what it always wanted: government approval and institutional credibility. President Trump has declared that he wants to establish the United States as the ‘crypto capital of the world.’ The U.S. has taken steps to integrate digital assets into the U.S. financial system and reduce regulations.

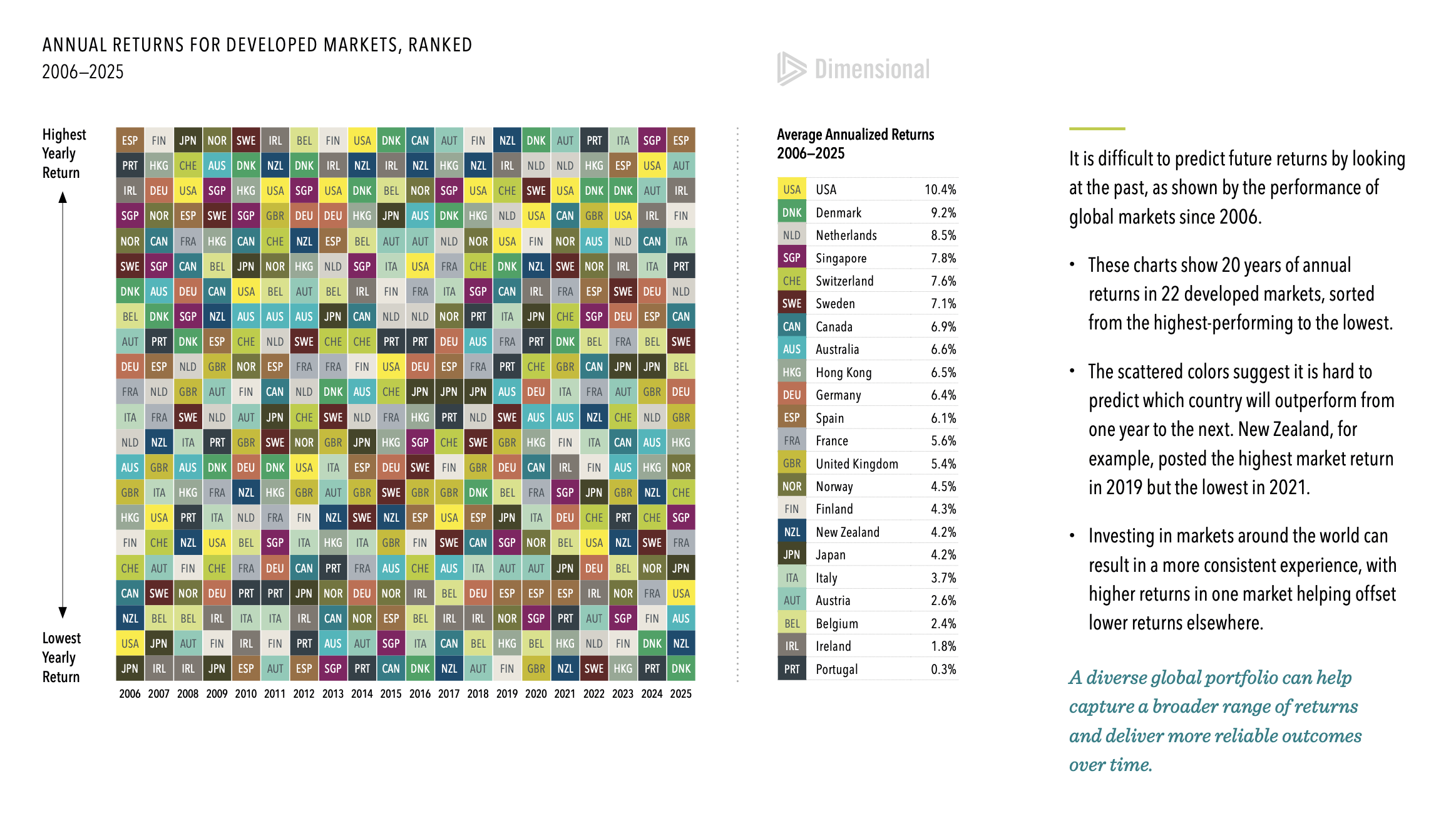

The Randomness of Global Stock Returns

It is difficult to predict future returns by looking at the past, as shown by the performance of global markets since 2006.

Dimensional Crosses $1 Trillion in Global AUM

On February 6, 2026, Dimensional reached $1 trillion (USD) in global assets under management. As we mark this milestone, we want to express our deep gratitude for the trust you’ve placed in us as stewards of your assets.

Why Prepare When AI will Take Care of Everything?

Should we all stop bothering to save for the future? Really? That sounds like a crazy idea, but it’s been proposed by none other than Tesla chairperson Elon Musk, in a recent podcast.

If You Think the Dollar is Weak…

How would you feel if an international financier offered to buy the coat off your back for 89,556 Lebanese pounds, or 42,112 Iranian reals? Would you jump at the offer? You shouldn’t. Those happen to be the two weakest currencies in the world today, and the mysterious financier’s offer would translate to a single U.S. dollar.

AI Inflation

The overall inflation rate has settled down to somewhere between 2.6% and 2.7%. But an unsettling trend might be building higher costs into our economy in two fundamental areas.

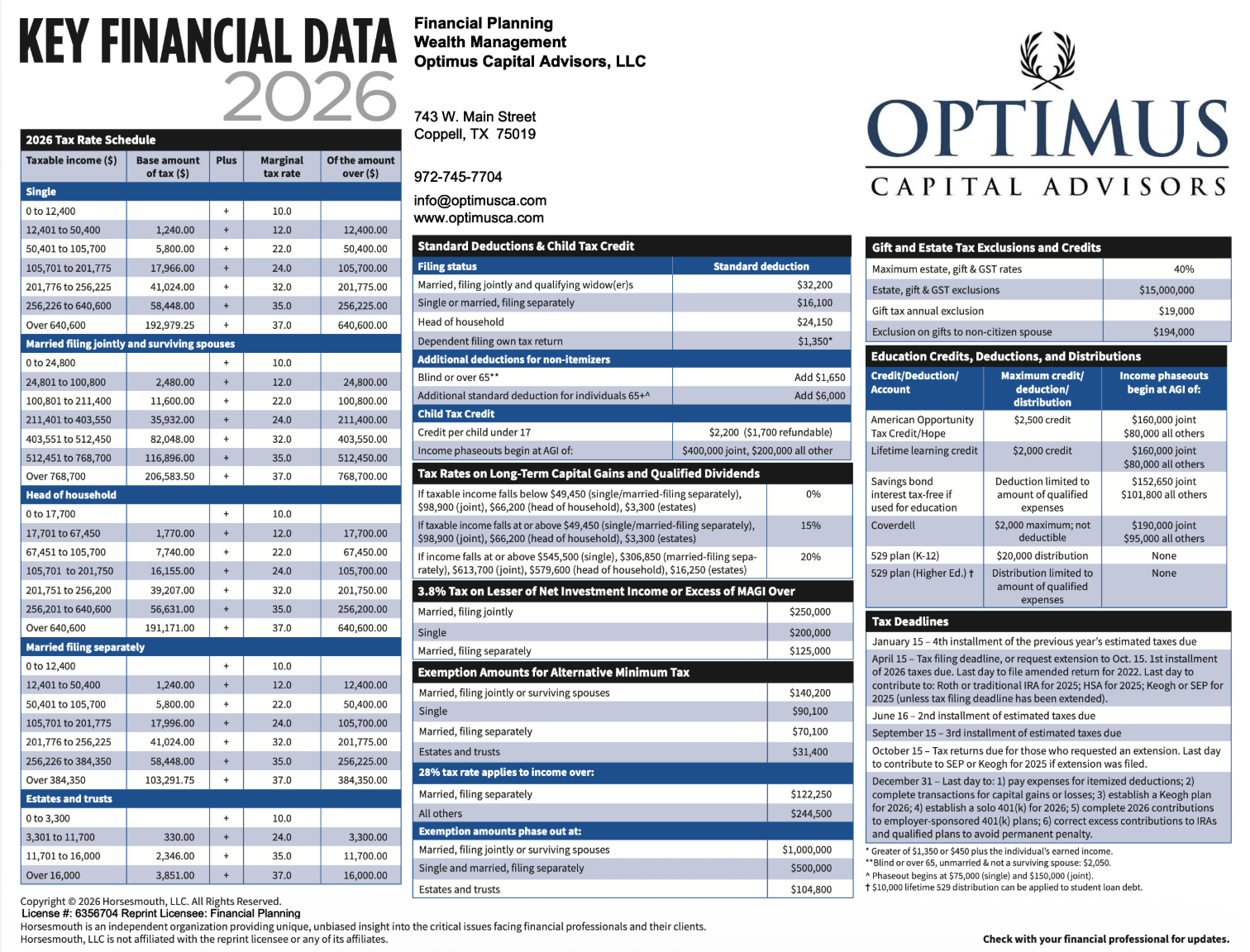

2026 Key Financial Data

Our team at Optimus has assembled key financial data worth knowing for 2026. You can download the file here.