Debt Up, Savings Down

According to the U.S. Bureau of Economic Analysis, today’s consumers, on average, are saving about 2.6% of their total disposable income. This is low by historical standards, and well below the 4.3% rate recorded in January. Back in 2023 and 2024, the rate was a much healthier 6%.

Economists get nervous when the rate is too high or too low. Too high, and it means that consumers aren’t buying goods and services—and consumer spending makes up around 70% of the economy’s overall growth. The economy could suffer a recession.

Too low, and it means that people might have trouble making their debt payments, generating a potential debt crisis that could lead to bankruptcies and… a recession.

How likely is it that debt scenario? It turns out that total debt liabilities among U.S. households has grown to a record $19.9 trillion—a sign that Americans are borrowing to fund their spending. On average, the 133.7 million households each owe roughly $150,000 in debt. (Of course, that varies per individual household.)

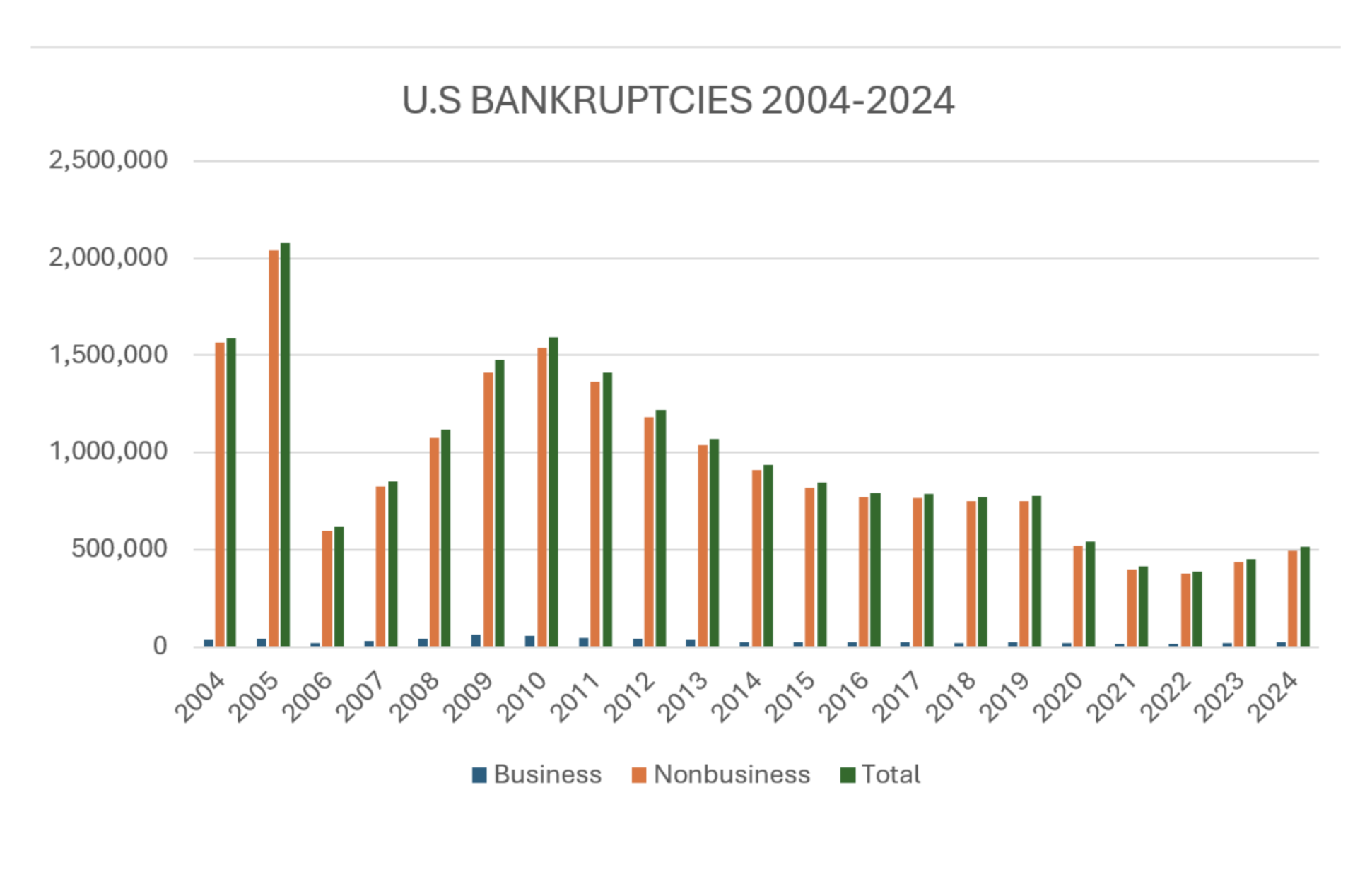

Is there any sign of growing bankruptcy activity? According to Debt.org, the number of people seeking debt relief in the courts grew 26.8% from 2023 to 2025, and bankruptcies through the end of March were up another 11%.

You can see on the chart, which only covers data through 2024, that the bankruptcy phenomenon tends to be somewhat cyclical. From 2006 through 2010, bankruptcies rose, then fell through 2022. They’re on the rise again, and if they follow a similar pattern, we could experience a recession in a year or two.

How could the U.S. avert that scenario? An economist would tell you that people should save more, and spend more, and pay down more debt. Good luck trying to put that into practice.