Debt and Politics

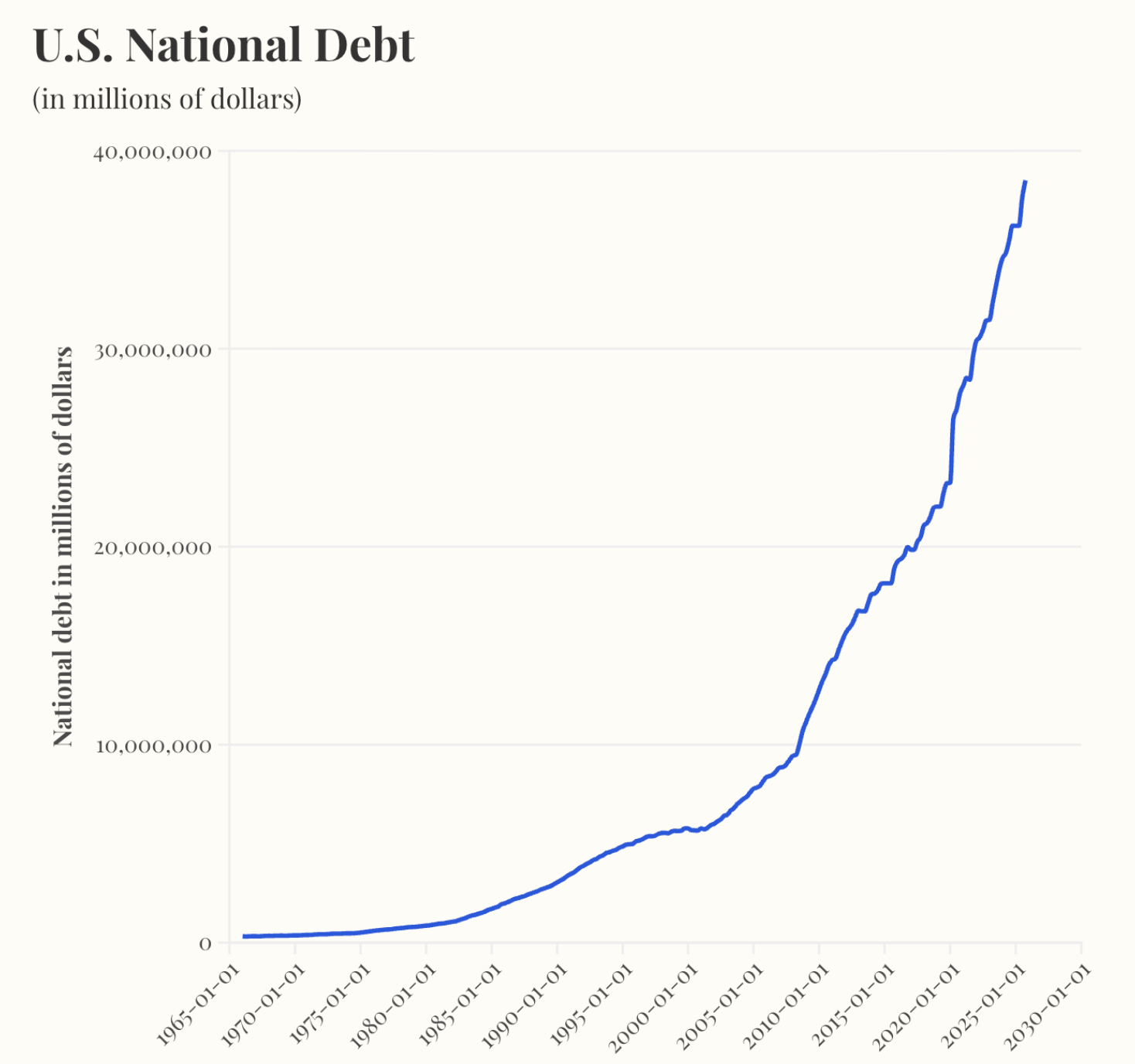

Looking ahead to the November elections, one headline that is bound to surface is the national debt. According to the Peterson Foundation, the U.S. debt figure will pass $40 trillion by November, and is now growing by roughly a trillion dollars every five months. Last month, the Congressional Budget Office estimated that this year’s balance sheet alone will bleed red to the tune of $1.9 trillion. Under current law, the annual debt increase will come to $3.1 trillion in 2036.

Interest payments represent the fastest-growing ‘government program’ in the federal budget. Over the first three months of the current year, the government will have paid $270 billion in interest on its debt, which is a higher number than the nation’s defense spending for the same period. And if one adds in other long-term government obligations like the promises to make Social Security payments and cover health costs through Medicare, the true fiscal gap exceeds $100 trillion.

There are two implications to this. The first is that whatever party is in power after the elections will be in a no-win situation; the only way out of the fiscal mess is to cut government expenses (meaning programs) and, at the same time, raise taxes. That would almost certainly result in a recessionary period as the markets and economy adjusts to awful-tasting medicine.

The other is that the combination of a recession and reduced government spending can lead to a downward spiral. The government’s normal process for reducing the impact of a recession is to ramp up spending—obviously not an ideal solution when the goal is to reduce the debt. And, of course, a recession often entails lower tax collections, since there are fewer profits and often less wages to tax. That might further exacerbate the debt situation, just in time for a new President to inherit an awful mess with no obvious solution.